Navigating the NACHA 2026 Changes: What You Need to Know

I remember the first time a payment I knowingly approved turned out to be part of a scam. No password was stolen. No account was hacked. I simply trusted the wrong request.

That moment captures exactly why the upcoming NACHA 2026 changes matter. These rules aren’t just about faster payments or tighter controls — they signal a fundamental shift in how trust, responsibility, and fraud prevention will work in the U.S. banking system.

A Shift in the Financial Landscape

For years, banks have played the role of efficient processors — moving money quickly and reliably through the Automated Clearing House (ACH) network.

But 2026 changes that equation.

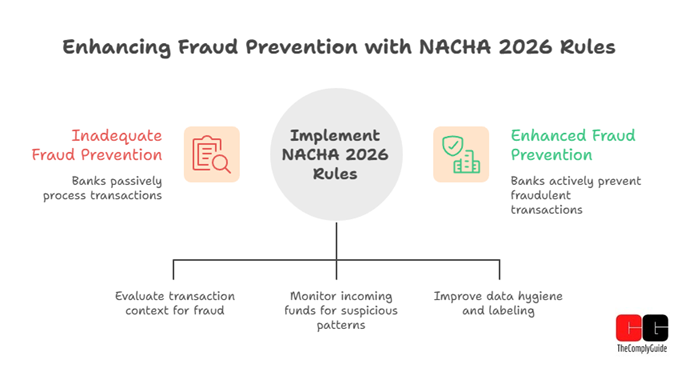

Banks are no longer just “plumbers of payments.” They are becoming risk evaluators — expected to assess not just whether a transaction is valid, but whether it should happen at all.

This shift is driven by a simple reality: fraud has evolved.

Gone are the days when fraud meant stolen passwords or hacked accounts. Today’s scams are far more sophisticated — social engineering, impersonation, and psychological manipulation. In many cases, customers themselves initiate the payment… just under false pretenses.

Imagine this: instead of simply verifying credentials, your bank pauses and asks —

Does this transaction make sense based on this customer’s behavior?

That’s the new world NACHA is building.

Redefining Transaction Authorizations

One of the most transformative elements of the 2026 rules is the concept of credit push transactions.

On the surface, this sounds empowering — customers actively authorize payments rather than relying on backend validation. But beneath that lies a deeper implication:

👉 Authorization no longer equals legitimacy.

In the past, if you approved a transaction — even under a scam — the liability often rested with you. The logic was simple: you authorized it.

Now, that logic is being challenged.

Under the new framework, banks are expected to detect and intervene in suspicious transactions — even if they are technically authorized.

Think of it this way:

If a scammer convinces you to send money to a “vendor” that doesn’t exist, the responsibility increasingly shifts to the bank to recognize unusual patterns and step in.

This is a major philosophical shift — from customer responsibility to institutional accountability.

Increased Responsibility for Banks

With that shift comes a significant operational burden.

Banks will now need to go beyond surface-level verification and dive into:

- Behavioral patterns

- Transaction context

- Historical activity

- Network-level signals (like money mule behavior)

For example:

If a personal account suddenly starts receiving multiple payroll-like deposits — that’s no longer just “unusual.” It’s a potential red flag that must be investigated.

In essence, banks are being asked to build systems that don’t just see transactions, but understand intent.

And that’s not easy.

It requires:

- Advanced analytics

- Real-time monitoring

- Cross-system intelligence

- And increasingly, AI-driven fraud detection

The analogy here is powerful:

Banks are moving from being security guards at the door to investigators inside the building.

Enhanced Data Hygiene and Compliance

Another critical — and often underestimated — change lies in data standardization.

NACHA is pushing for better data hygiene, requiring more structured and descriptive transaction information. For instance, labeling payments clearly as “payroll” or “vendor payment.”

Why does this matter?

Because better data enables better detection.

If systems can clearly distinguish between transaction types, they can identify anomalies faster — like a “payroll” payment being sent to an unrelated personal account.

But this also introduces new challenges:

- Legacy systems may struggle to adapt

- High-volume banks will need real-time processing upgrades

- Smaller institutions may face resource constraints

And then there’s the risk of overcorrection.

Too many false positives could lead to:

- Delayed transactions

- Customer frustration

- Erosion of trust

Compliance, meanwhile, is non-negotiable. Penalties for non-adherence could include fines or even restricted network access — a serious consequence in today’s digital-first banking ecosystem.

A Phased Approach to Rule Changes

To ease the transition, NACHA is rolling out these changes in two phases:

- March 20, 2026 → Large, high-volume financial institutions

- June 19, 2026 → Smaller banks and credit unions

But here’s the catch:

There’s no real “soft landing.”

From day one, institutions are expected to comply.

This creates a high-pressure environment where banks must simultaneously:

- Upgrade systems

- Train teams

- Implement monitoring frameworks

- Ensure regulatory alignment

It’s less of a gradual rollout and more of a controlled sprint.

Those who execute well will gain trust and competitive advantage. Those who don’t may face both regulatory and reputational risks.

What Does This Mean for the Banking Environment?

As these changes take effect, the banking experience itself may begin to feel different.

Safer? Almost certainly.

More controlled? Very likely.

There’s an interesting tension here — one that mirrors a familiar dynamic:

👉 Protection vs. autonomy

Banks, in their effort to prevent fraud, may introduce friction:

- Transaction delays

- Additional verification steps

- Behavioral checks

While these measures enhance security, they also raise important questions:

- Will customers feel overly monitored?

- Will convenience take a backseat to compliance?

- Can banks strike the right balance between trust and control?

This is where the real challenge lies — not just in implementing the rules, but in designing an experience that still feels seamless.

Conclusion

The NACHA 2026 rule changes are not just regulatory updates — they represent a structural shift in how digital payments are governed.

Banks are moving from passive processors to proactive protectors.

Customers are moving from sole responsibility to shared accountability.

And the entire system is evolving to keep pace with a new generation of fraud.

As this transformation unfolds, one thing is clear:

The future of banking won’t just be about moving money faster —

It will be about moving money smarter, safer, and with greater awareness than ever before.